The Global Conundrum

A few thoughts

US

US indices are currently seeing downward pressure related to uncertainty brought on by the extension of the government shutdown, which now sets a record for the longest shutdown today. The Dems recent wins in mid-term elections have strengthened their holdout position as they vie for more leverage with Republicans. Trump essentially blames the shutdown for the Dems success, which seems to hint that the TACO effect could be underway although today Trump appealed the Supreme Court’s ruling that his admin must fund SNAP which points to a potentially longer stand still. Markets need to see the gov’t shutdown layer of uncertainty removed to gauge risk-taking prospects and money will likely remain sidelined until then, giving the Bears the impetus to control the narrative. Markets have ignored strong earnings this week while punishing underperformers, which seems to show that there’s a liquidity drain caused by sidelined money due to the uncertainty of the shutdown. Powell’s hawkish Oct cut did not help, especially since he mentioned that the lack of data reporting and uncertainty is likely to lead to a Nov rate hold, although markets are pricing in about 72% odds of a 25-bps cut. Now that the SPX is below the 21-day EMA, with the 8w-EMA sitting near 6,685, it’s key to watch MAs for support and if the 8wk-EMA breaks decisively, I’d look to the 50-day MA near 6,665 or the Aug high near 6,500 as the next likely areas of support. With ES Futures bouncing at the 8w-EMA as I type, I’m curious to see if we get an overnight reversal in trend, possibly on anticipation of gov’t shutdown capitulation. The 8w-EMA has provided strong support since May and if it breaks that would be a strong case for more downside. As far as the worries regarding AI/DC over commitments, I’d like to see investments expand to other regions of the globe and collaborations and investment partnerships between the US and other nations to increase energy capacity, and to shift investment risk from US Hyperscalers to sovereign developments. One option is to avoid placing the bulk of AI/DC credit risk on the U.S. Instead, the U.S. may need to revise its export license policies to enable AI/DC investments and commitments in other countries, helping diversify buildout risk.

EU

The EU has remained in a position on certain uncertainty, involving the conundrum of a German fiscal push, volatile inflation, a small upside surprise to GDP, and ECB hawks. The ECB’s October meeting offered limited guidance to markets, as President Lagarde highlighted uncertainty as the main factor of the board’s decision and guidance which signaled a hawkish cut. The limiting nature of the region’s regulatory structure have limited growth and investments, and it appears going forward, the rate of growth will be largely dependent on the success of Germany’s fiscal package. I wouldn’t be surprised to see the region’s performance go from leader in ’25 to laggard in ’26.

China

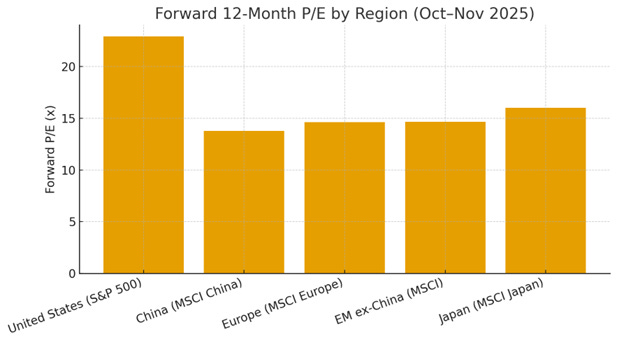

I’m under the impression that China is set to outperform in 2026 largely because of their energy abundance and consistent signals of increased confidence in their domestic semiconductor capabilities. China trades at a 40% discount to the S&P 500 on forward earnings. Although the lower valuation reflects heavy state-owned enterprise exposure, policy risk, and weaker profitability vs. US Mega Cap Tech, it appears that the gap should close 15-20% due to China’s superior position in energy to back AI/DC commitments. Certain provinces have elected to offer China’s tech companies 50% cost reductions on electricity costs, on the condition that they use domestically manufactured semiconductors. In Shanghai and Chengdu officials are offering small-medium enterprises subsidies covering up to 80% of AI rental/training compute costs for eligible users. The point being that when considering Jensen Huang yesterday saying that “China is going to win the AI race” going on to say that “power is free” in contrast to high energy cost in the US.

India

I’m starting to consider India as a focus point of investment and when considering the region’s underperformance YTD, 7%+ estimated GDP growth, and Trump stating today that talks with India are going well and Modi is “great”, I think India could be a potential underperformer to outperformer in 2026 due to their access to cheap energy making them an attractive investment for DC buildouts. India’s 2025 budget policy adds tax breaks and cheap power for DC investments.

Just a few thoughts heading into the end of the year. Thanks for following.