The Setup

Markets are starting to settle into the fact of Trump uneasiness brought on by the early April bond volatility. Trump may not want to admit it, but the uncertainty brought on by his tariff policy has called the US’s reliability and credibility into question and once the bond market spoke Trump has since softened his rhetoric. The lingering questions will revolve around the extent of damage that has already been done and the policy path forward. As hard data comes in markets will either continue to climb a wall of worry or decline/price in bigger odds of recession if/once we see hard data begin to turn over. At this time, hard data continues to hold up as can been seen below in the summary of this week’s data releases. Goin forward, we have Non-farm Payrolls data releasing this Friday which should be interesting after we saw jobless claims/continuing jobless claims data come in above consensus today.

I’m particularly wary of the election gap on SPX between 5780-5860 as a likely spot of resistance IF SPX can push past the Summer 24’resistance TL near 5670. If we stall out here below 5670, we will likely see SPX back test 5500 as prior resistance flipping to support. The next major catalysts likely to move the index are the usual tariff headlines, tax reductions, and de-regulation in addition to hard data. With positioning as washed out as it has been over the past two months, it continues to seem like the pain in trade is markets climbing a wall of worry. Wouldn’t be surprised to see a chase lead to a test of the election gap which is a likely spot many will cut recent winners off the 4800 bottom. I wouldn’t be surprised to see SPX form a handle right hear as it tests 5670 with the bottom of the handle potentially landing at the 8-day EMA near 5500. The 5500 TL also coincides with a 50% retrace of the ATHs/4800 range, making it a particularly interesting point of confluence sitting right near the 8/21-day EMAs.

SPX

Parsing through the daily rhetoric to gauge what direction policy may be headed continues to be the toughest game going forward. Overall, the rhetoric coming from the Trump administration has softened substantially while other nations have taken a more hardline stance. I’ve never read The Art of the Deal but I’m under the impression that Trump’s deal making strategy has worked against him so far and instead of caving in, the hawkish rhetoric has led other nations to take a defensive posture. Going forward, the direction of policy hinges on Trump’s rationalization and realization that policy implementation requires clear and concise planning and messaging. For the most part, it seems this reality has led to the “Trump put” being enacted in abundance of caution towards the reverberations of sloppy policy in the bond market. We shall see.

One fact that remains is that the fiscal deficit is out of control. With this administration aiming to reduce taxes, it doesn’t look as if the deficit will be addressed anytime soon. I think this administration is privy to the fact that real spending cuts equal a recession and tariff revenue will be an unlikely source of reprieve. This creates a bad mixture of deficits potentially blowing out, sending bond yields higher all the while the US pays record levels of interest which some estimate could reach a third of GDP by 2030. I’m aiming to take a TLT short for this reason hopefully on a flush of the10Y to 4%. I could see TLT testing those Oct ’23 lows near 82.50 in this case once investors wizen up to the fact that the US refuses to force a self-induced recession through fiscal responsibility while Europe/China stimulate their economies.

10Y

TLT

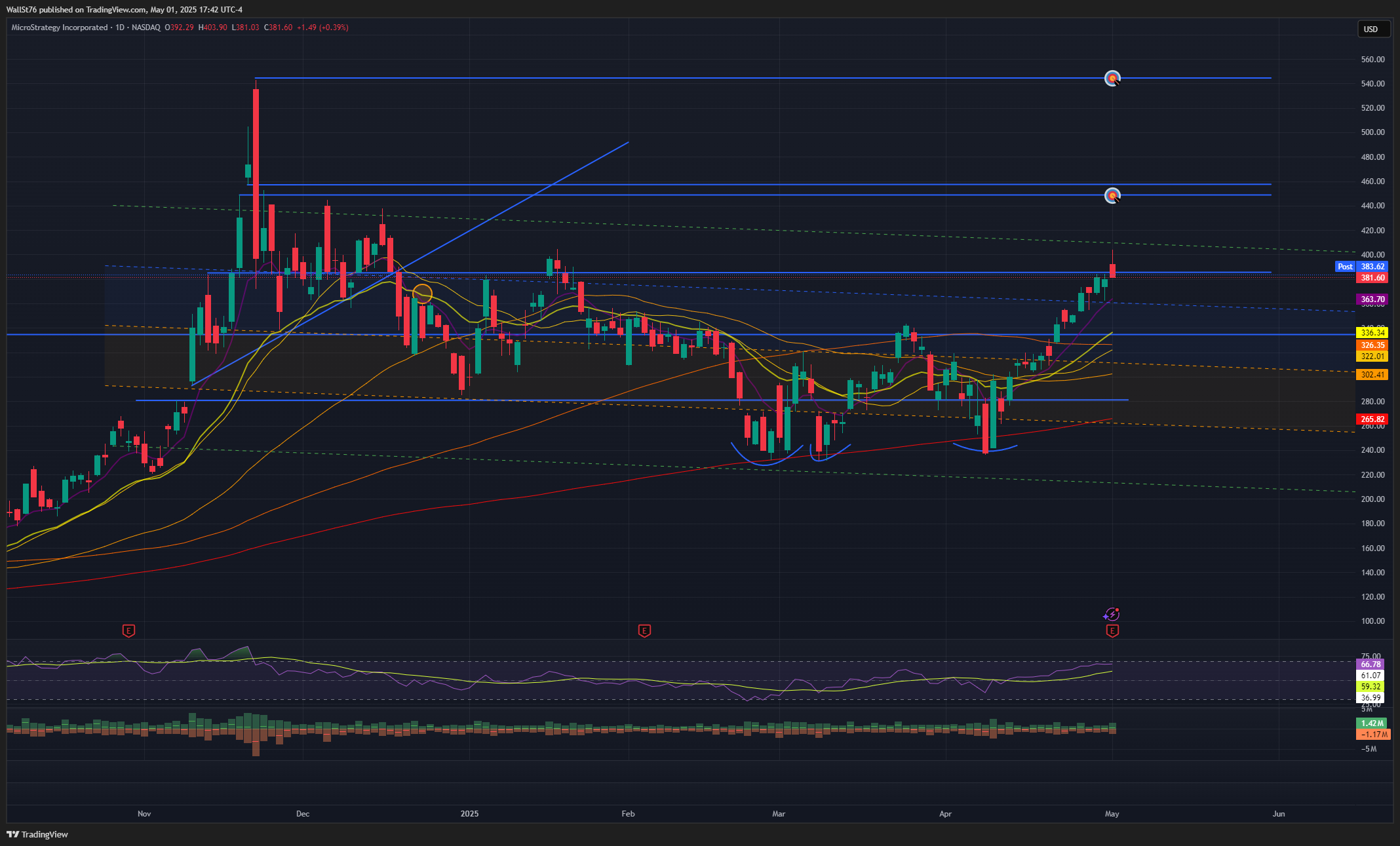

I continue to like the BTC and MSTR here. Today MSTR announced a BTC Yield of 13.7% and a BTC dollar gain of $5.8B year-to-date. MSTR doubled their capital plan to $42B equity and $42B fixed income to purchase bitcoin and increased their BTC Yield target from 15% to 25% and BTC dollar Gain target from $10B to $15B for 2025. BTC looks strong technically and has recently played hedge to geopolitical uncertainty/de-dollarization while also offering risk on upside. Therefore, no matter whether you subscribe to the end of US exceptionalism theme, continued tariff uncertainty, or expect markets to continue climbing a wall of worry, it seems as if BTC/MSTR may work in any of these scenarios.

BTC Weekly

BTC Daily

MSTR

That wraps up this mid-week letter. Thanks for reading.

**Disclaimer**

The content provided on this Substack is for informational purposes only and should not be construed as financial or investment advice. The information is provided on an "as is" basis with no guarantees of completeness, accuracy, usefulness, or timeliness.

The author(s) and publisher(s) are not registered financial advisors. The ideas, strategies, reports, articles, and all other content on our Substack are provided for informational and educational purposes only and should not be construed as personalized investment advice.

Investments in the securities markets, and especially in options, are speculative and involve substantial risk. Only you can determine what level of risk is appropriate for you. Prior to buying or selling an option, an investor must receive a copy of Characteristics and Risks of Standardized Options.

We do not promise or guarantee any income or particular result from your use of the information contained herein. Past performance is not indicative of future results. It should not be assumed that future picks will be profitable or will equal past performance.

By reading this Substack, you acknowledge and accept that all trading decisions are your own sole responsibility, and the author(s) or anyone associated with this Substack cannot be held responsible for any losses that are incurred as a result.

I love these thought pieces

Was eyeballing TLT short a bit higher as well. BTCUSD continues to chug away!